IFRS 16 Overview

Everything you need to know about IFRS 16

The financial statement fraud in Enron, WorldCom and others were drivers to the creation of the new IFRS lease accounting standard. IFRS 16 closed the loophole which allowed corporations to hide certain assets and liabilities off-balance sheet. Under the standard, companies are required to capitalize most leases on the balance sheet — reporting them as right-of-use assets and lease liabilities. As a result of the shift, capitalized lease obligations face increased auditor scrutiny, pushing companies to focus on ensuring accuracy and completeness of what they report as well as leading to greater transparency and comparability of financial statements.

Keeping operating leases off the balance sheet is believed to obscure the true nature of a company’s liabilities from potential investors. To increase transparency into corporations’ true lease liabilities, the International Accounting Standards Board (IASB) developed a new standard that eliminated the operating lease classification.

In 2019, the latest IASB lease accounting standard, IFRS 16, began to go into effect for companies worldwide. Among other requirements, IFRS 16 required that most leases be capitalized and recorded on the balance sheet, changed how they’re reported, and eliminated most operating (non-capitalized) leases. According to the American Institute of Certified Public Accountants (AICPA), approximately 90 countries have now adopted IFRS. Aligned closely to IFRS 16, there are many country-specific versions, including AASB 16 in Australia, NZ IFRS 16 in New Zealand, FRS 116 in Singapore, HKFRS 16 in Hong Kong, and K-IFRS 16 in South Korea.

Handbook

This is a brief introduction to IFRS 16. For more detail on the technical accounting as well as how companies can successfully achieve and maintain compliance with the standard, download our full IFRS 16 Handbook.

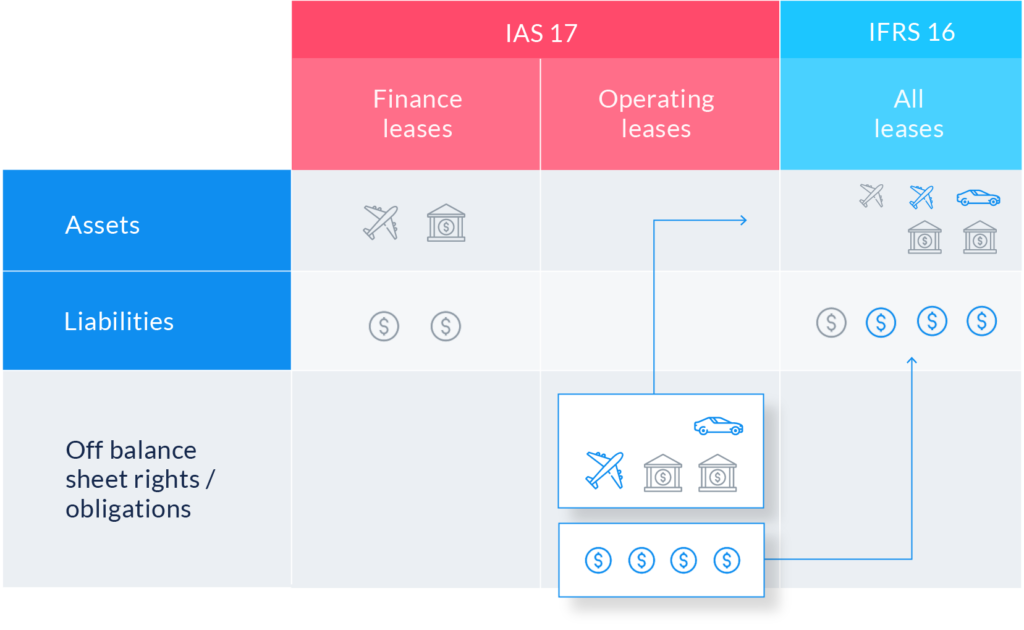

The most notable change is the elimination of the operating lease classification. Under IFRS 16, all leases, excluding those that meet the practical expedient for low-value and short-term leases, if elected, are treated as finance leases. The lease assets and liabilities are recognized on the balance sheet, which may result in a significant increase in the amount of assets and liabilities many companies report. Finance leases are also reported differently on the profit and loss (P&L) statement than operating leases under the previous standard. Operating leases were reported as a straight-lined rent expense. However, under IFRS 16, all lease expenses are reported as a separate (usually straight-lined) amortization expense of the asset and a declining interest expense based on the liability being reduced with periodic payments. As a result of the standard, the lease expense will likely impact financial metrics such as EBITDA, as amortization and interest are excluded from the EBITDA calculation while the lease expense is included.

The IASB also considers leases to be debt, and as such, debt to equity ratios may see a dramatic increase. This could impact debt covenants not covered by frozen GAAP contractual provisions as well as credit ratings, if the lease liability recognition resulting from the adoption of IFRS 16 is significantly different from analysts’ expectations. The ROU Asset is an intangible asset where the liability is tangible, and accordingly may affect asset ratios as well. Lastly, remeasurements of the lease liability are required due to changes in variable rents, such as those based on an index or rate.

We’ve built a set of lease accounting examples to help you get started. Use our free IFRS 16 lease accounting examples below to understand how the standard works or see the ASC 842 journal entries in real-time in our free trial.

Businesses need to consider other implications that this standard has triggered, such as:

After the accounting scandals of the early 2000s, there was a major push by the accounting standards boards to close accounting loopholes and increase transparency into the true financial position of corporations.

One of the loopholes identified was the operating lease loophole under IAS 17 which allowed companies to report operating leases in the notes of financial disclosures. To close that loophole and increase transparency, the IASB released IFRS 16 in January of 2016.

IAS 17 Leases (1997) is the previous lease accounting standard for all companies that report under international financial reporting standards. IAS 17 used a dual-model classification approach. One classification, finance leases, was capitalized on the balance sheet as an asset and liability and reported on the P&L statement as an interest and depreciation expense. The other classification, operating leases, was reported in the notes of financial statements.

IAS 17 Accounting for Leases (1982) was issued with an effective date of 1 January 1984.

The Group of Four Plus One (G4 + 1) which includes Australia, Canada, New Zealand, the United Kingdom, and the United States plus the IASB published a discussion paper for a converged standard for lessees which called for the elimination of operating leases.

IAS 17 Leases (1997) was issued with an effective date of 1 January 1999. This superseded the previous IAS 17 Accounting for Leases, of 1984. Under IAS 17, leases had to be classified as either operating leases or finance leases. Operating leases were reported as an expense on the income statement and in the notes of financial disclosures. Finance leases had to be reported as an asset and liability on the balance sheet.

G4 + 1 began work on a converged standard for lessors building on the 1996 discussion paper.

The IASB began work on a new lease accounting standard intended to close the loophole of off-balance operating leases.

The IASB released a Discussion Paper covering preliminary views on the creation of a new lease accounting standard and invited comments. The discussion paper proposed moving all leases onto the balance sheet to be capitalized as an asset and liability.

The IASB released the first Exposure Draft for the new lease accounting standard and invited comments. The draft established the model to report all leases on the balance sheet as an asset and liability. In general, this model was met with criticism.

The IASB released the second Exposure Draft after multiple discussions with stakeholders and several revisions. This model solidified parts of the new standard, including the model to bring all leases, except short-term leases, onto the balance sheet.

The IASB released IFRS 16 (eIFRS login required) in January of 2016 with an effective date of 1 January 2019.

Use this short tutorial to see how to account for an operating lease.

Learn about how to adopt the standard and make your implementation successful.

Optimise long-term compliance with the right approach.

If you’re still using spreadsheets, for lease accounting, it’s time to change.

Use this short tutorial to see how to account for a capital lease.

Use this short tutorial to see how to account for a finance lease.

Use this short tutorial to see how to account for a finance lease.

Related sites

Site architecture

© 2024 EZLease Lease Accounting Software by LeaseAccelerator. Copyright 2000-2024 LeaseAccelerator, Inc. All rights reserved. The other logos (brand identities) presented on this website are property of their respective owners.